Your credit score is one of the most important pieces of your financial puzzle. It’s a number that lenders look at to determine your creditworthiness and can impact everything from the interest rate you’re offered on loan to whether or not you’re approved for a mortgage. So, how often should you check your credit score?

Your credit score is one of the most important pieces of your financial puzzle. It’s a number that lenders look at to determine your creditworthiness and can impact everything from the interest rate you’re offered on loan to whether or not you’re approved for a mortgage. So, how often should you check your credit score?

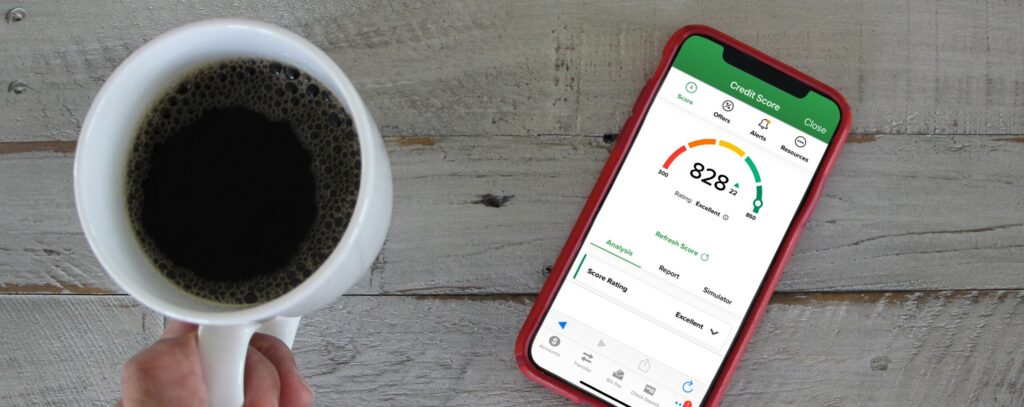

The answer may surprise you. Checking your credit score too often can have a negative impact on your score. That’s because each time you check your score, it’s recorded as an inquiry on your credit report. And too many inquiries can hurt your score. So, how often should you check your credit score? The best practice is to check it once a year.